Cash is fuel.

As a tech company CEO, you need cash to scale. Most small businesses in the United States generate cash from operations. There’s nothing wrong with a self-funded business. You retain full ownership, free to chase your dreams as you want without any anxious investors to deal with.

It’s not so easy for technology companies. Tech moves too quickly. A self-funded tech company is at risk of being eclipsed by a well-funded competitor. For this reason, most promising technology companies pursue outside funding to accelerate business growth.

Funding is the fuel you need to scale your company and to exit at a time and on terms of your choosing. So how do you get funded? Fundraising is both an art and a science. You weave strands of traction and the swatches of opportunity into a beautiful tapestry — your “epic story”. That’s the art. But surrounding that art is a lot of science. Here, you will learn how to time your fundraise, how to execute it, and eventually, how to sell your company at maximum valuation. All three of these things are important. Your family, your employees and your previous investors count on you to do them well.

What makes you, as CEO, investable? What progress must you prove and what potential must you show? How do you target the right investors, given your progress? What preparatory steps must you complete before you start working on the pitch? How exactly do you prepare your story so that the elevator pitch, the executive summary, the pitch deck, the demo, and the Q&A talking points are all fully aligned? What alternative funding sources are available to you? What motivates each of these investor types? The answers to all these questions are in this book.

Successful fundraising requires smart timing. It’s critical to plan thoughtfully, so that you reach an investment-worthy value inflection point well in advance of each funding event. The journey from first preparatory steps to final close and cash in the bank can take months. As CEO, it’s on you to ensure you close each funding event with cash to spare.

There is an investor class for every stage of company growth. The investment thesis, risk profile and expected return vary for each. In Funding & Exits, you’ll learn about each investor class. Armed with this knowledge, you can match your company’s progress to the right investor class. Nothing wastes more time than chasing investors who have zero chance of investing in you. Your investor search must be efficient and effective. Remember, time is not your friend. Every day, cash burns.

Investors buy stories. The fundable story wins on two dimensions: opportunity and traction. Opportunity — the investor’s judgment about your future performance — is demonstrated through your product vision and road map, your competitive advantage thesis, your market opportunity thesis, your business model, your go to market strategy, and (perhaps most important of all) your team. Traction is proven by the achievement of value inflection points, specifically in the domains of product, revenue engine, systems, people, and cash position.

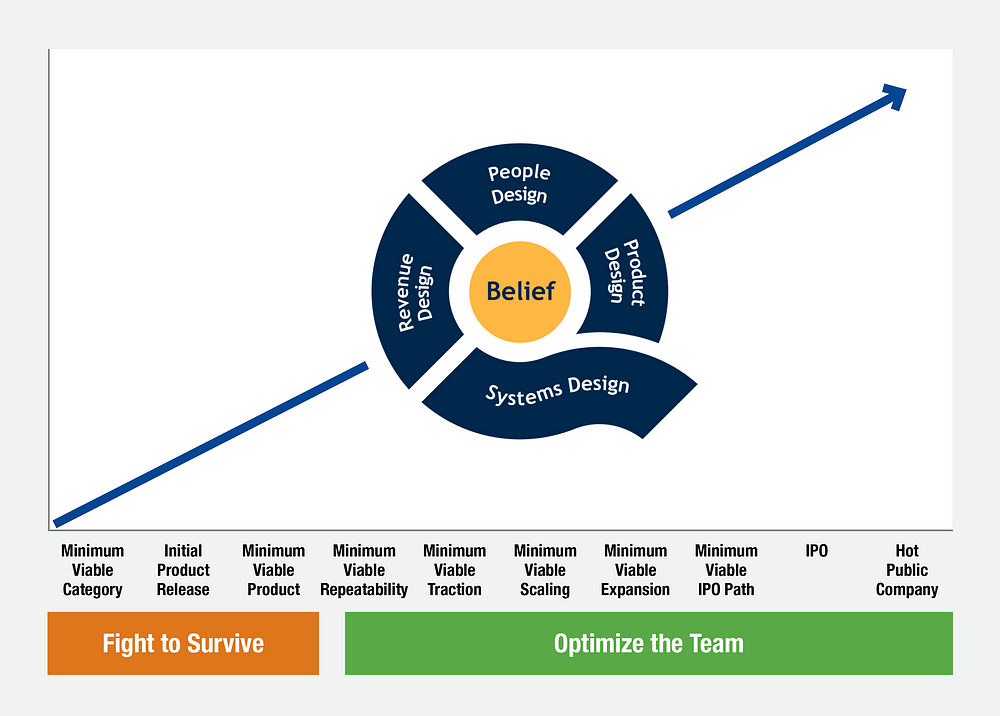

Value inflection points are the milestones a company must achieve in order to be fundable. These are the points in the journey where a company’s investment value jumps due to a newly achieved proof of traction. The initial product release is a value inflection point. So is Minimum Viable Product, Minimum Viable Traction, Minimum Viable Scaling, and — at the later stage of a company — the IPO. Your investment story is anchored by the value inflection point you have most recently achieved. Funding follows milestones. Are you clear on the milestone you have achieved? Do you understand which investor class is most relevant, given that milestone? Have you leveraged that knowledge to choose the right investor class, create the list of appropriate target investors, and prepare your “opportunity and traction” story?

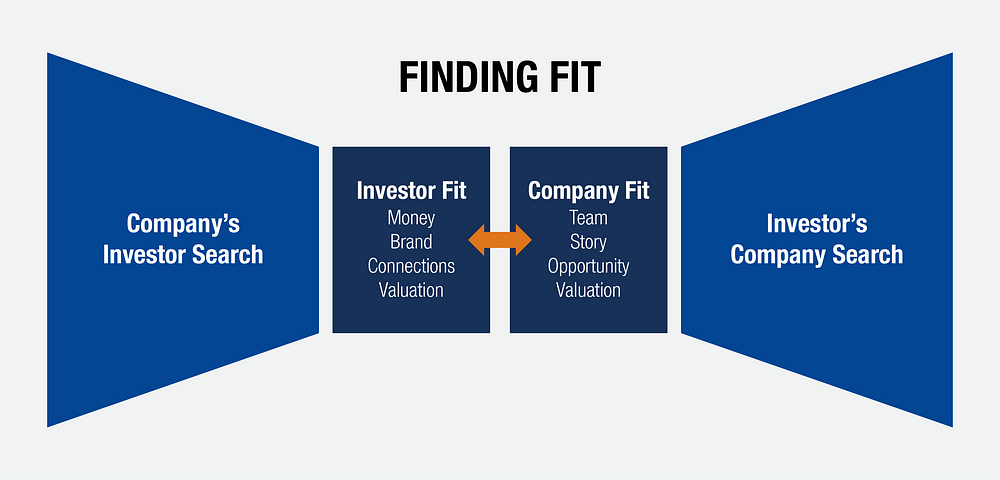

Funding happens when both company and investor decide they are the best fit for each other, compared to all other alternatives. At every stage of the funding process, companies and investors seek similar things:

- Lots of top-of-funnel optionality

- Efficient “not interested” communications

- A partner that meets pre-determined attributes for fit

- Open consideration of multiple alternatives, even if interested

- Efficient mutual valuation

- Enough diligence to validate claims while not slowing things up so much it costs the deal

- Thorough but efficient negotiation of terms

- Thorough but efficient finalization of definitive documents and close

- Commitment to the company through thick and thin

- Celebration of a successful exit

The most promising tech companies are able to be picky about their investors. For such companies, cash and a favorable pre-money valuation are not enough. Company CEOs will favor the investor who boasts lots of dry powder to follow on in subsequent rounds. She will favor the investor with an elite brand, who brings relevant domain expertise and can leverage powerful connections. Investors such as these help a company scale faster, find more powerful partners, raise more money, experience less dilution and accelerate towards outsized exits.

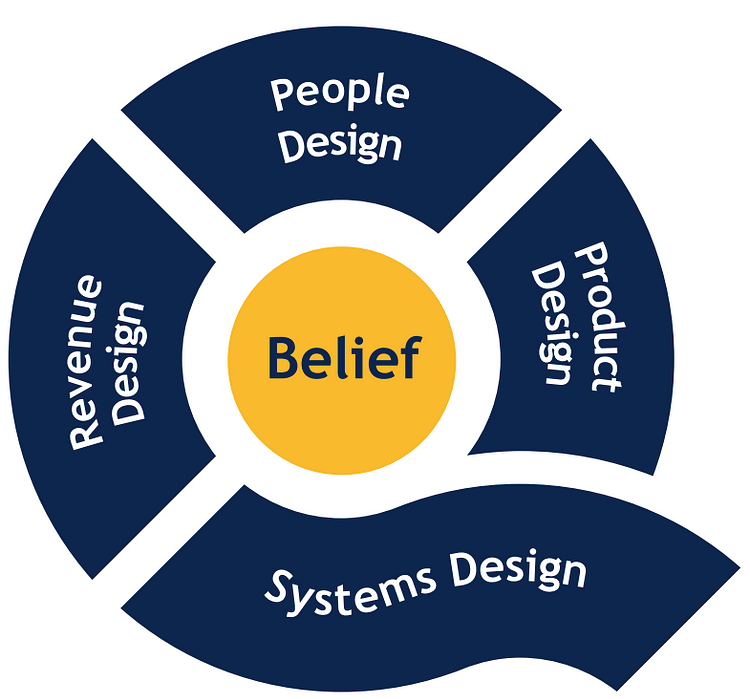

At my company, CEO Quest, we believe that company building occurs in five domains, represented by the CEO Quest “Q”.

Funding and Exits is the third in a series of five books, which match the five company building domains. My first book was Scaling the Revenue Engine. My second was People Design. Two more are planned. Here in Funding & Exits, our focus is on the center circle, Belief.

Belief is the domain of “what you believe”, and “who must believe”. “What you believe” refers to your vision, your mission, your values and your strategy. “Who must believe” refers to customers, employees and investors.

Yes, investment is belief, for in the act of funding a company, someone with money makes the formidable decision to part with it. Why? Because she has listened to your story and has come to believe in it, and in you. She has become convinced that an investment in your company will yield safety and return superior to any other alternative in her chosen investment class. In turn, you have chosen her to be the investor in your company. You too believe. You believe that she possesses the money, the investor brand, the connections and domain-relevant expertise to help you scale your business towards an exciting exit.

This is the journey of company building. At every stage, you must confront and crack the riddles presented in the five domains. None is more important than funding, for without cash you have nothing.

Over the past thirty years, the majority of highly successful technology companies have availed themselves of VC funding — including the biggest ones (Microsoft, Apple, Google and Amazon). But VC funding is not the only source of funds to scale. In the earliest stage of your company, there are angel investors, incubators, and accelerators. In later stages, commercial lending and venture debt come into play. Even later, hedge funds become viable funding sources. Eventually, for a very small number of companies, the public markets beckon.

Chapter 1 of Funding and Exits starts with you, the entrepreneur. What are the essential characteristics of an investable entrepreneur? What steps must you take to make yourself investable? In Chapter 2, you’ll learn about the value inflection points. From there, you’ll learn about the investor continuum — the investor classes available to you at each stage of growth. Then we discuss the art of storytelling, for indeed, investors buy stories. In Chapters 5 through 8, you’ll learn about every step of the funding process. After that, we’ll explore different investment types, from angel and incubator investments, to venture capital, to commercial lending, to venture debt. We explore the underlying investment thesis of each and discuss how to access the funding. Finally, in the last four chapters, we address the exit process and the exit paths, strategic acquisition, private equity and IPO.

Here is the table of contents:

- Chapter 1 — The Fundable Entrepreneur

- Chapter 2 — The Value Inflection Points

- Chapter 3 — The Investor Continuum

- Chapter 4 — Investors Buy Stories

- Chapter 5 — Startup Funding: from Inception to Term Sheet

- Chapter 6 — Startup Funding: the Term Sheet (Overview)

- Chapter 7 — Startup Funding: the Term Sheet (“Heads Up” Terms)

- Chapter 8 — Startup Funding: from Term Sheet to Close

- Chapter 9 — Incubators, Accelerators, Angels and Seeds

- Chapter 10 — Venture Capital

- Chapter 11 — Commercial Banking

- Chapter 12 — Venture Debt

- Chapter 13 — The Non-IPO Exit: Overview

- Chapter 14 — The Strategic Exit

- Chapter 15 — The Private Equity Exit

- Chapter 16 — The IPO Exit

Prepare well, and you are more likely to get funded — and on terms favorable to you. In preparing for funding, you strengthen your grip on the company’s future. The imperative to tell a convincing story about exactly how you will scale the company forces you to think it all through. Funding events make you a better CEO.

If you take this book seriously, you won’t forget about funding once you’ve closed a round. You will celebrate the wiring of funds, and then you’ll sharpen your line of sight to the next funding event. By understanding “what must be true” at every funding milestone, you can organize company priorities and plans accordingly. This planning-based approach to fundraising, always looking outward towards the next funding event, is a key lesson of this book.

Someday you and your investors will decide it’s time to exit. As with funding, you must manage the exit process with care. Start early by cultivating relationships. Know your options — from a private equity exit, to a strategic exit, to going IPO. Execute the process from start to finish with precision. How? Read the book — the answers are here.

I want to thank my son Jack Mohr, who provided extensive advice and counsel to me. Jack is equity analyst at the hedge fund EOS Partners in New York. Previously, he was co-portfolio manager of Jim Cramer’s charitable trust (along with Cramer himself), and was chief investment officer of TheStreet.com. Before that he worked in equity research at Barclays. In 2017, he attempted to launch a VC fund, which ultimately proved unsuccessful but was instructive to him, and by extension to me. Jack’s deep understanding of the value drivers that matter most in public company stock prices, his experience with IPOs, and his adventure into the world of VC finance made him a valued critic and contributor during my book writing odyssey.

My special thanks go to Bruce Cleveland, General Partner at Wildcat Ventures. His Traction Gap framework is the starting point for the value inflection point continuum shown in this book. The first five inflection points (Minimum Viable Category, Initial Product Release, Minimum Viable Product, Minimum Viable Repeatability and Minimum Viable Traction) are taken right out of Traction Gap, with Bruce’s permission. I have then extended the continuum, adding Minimum Viable Scaling, Minimum Viable Expansion, Minimum Viable IPO Path, IPO and Hot Public Company. Bruce was both generous and flexible as I built upon his original framework. Moreover, he has provided wide ranging feedback on the key attributes of a fundable entrepreneur and company.

Jason Green, founder and general partner at Emergence Capital, critiqued my venture capital chapter, making helpful edits. Steve Wurzburg, attorney at the firm Pillsbury Winthrop Shaw Pittman, provided invaluable insights for the chapters devoted to term sheets. Christian Bennett, managing partner at the investment banking firm Pagemill Partners, took time to critically evaluate the three chapters related to non-IPO exits. Bob Curley, Chief Credit Officer and Executive VP of Bridge Bank, opened the window into commercial banking and advised me on all the lending options available to tech startups. Rudy Ruano, Partner at Western Technology Investment, and David Spreng, CEO and CIO at Runway Growth Capital, both provided helpful insights into the world of venture debt. SC Moatti, Managing Partner at Mighty Capital and an active angel investor, provided excellent input for the chapter on angel investing, as well as the venture capital chapter.

I am grateful to have had the support of such distinguished and thoughtful advisors; their feedback has been invaluable.

. . .

To view all chapters go here.

If you would like more CEO insights into scaling your revenue engine and building a high-growth tech company, please visit us at CEOQuest.com, and follow us on LinkedIn, Twitter, and YouTube.